and the distribution of digital products.

State of Sia Q3 2024

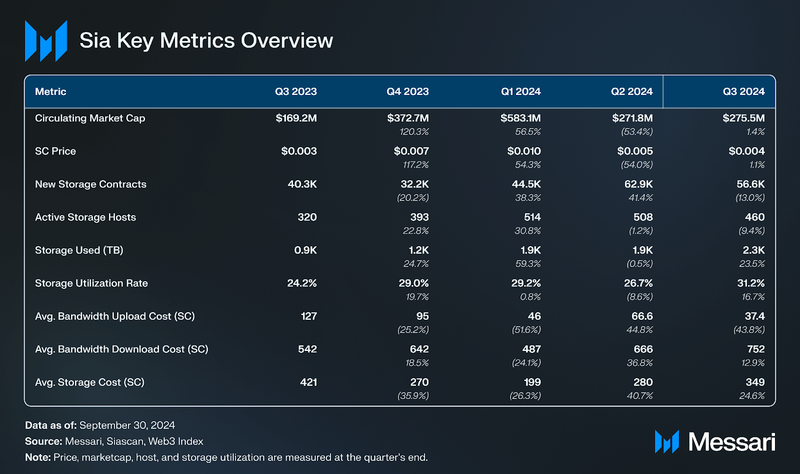

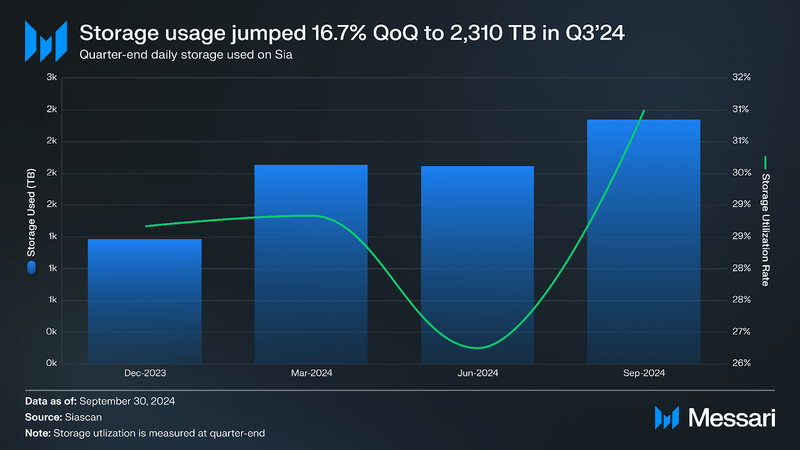

- In Q3’24, storage usage rose 16.7% QoQ to 2,310 TB, reflecting an increase in the network’s storage utilization rate and an emerging shift in user demand toward storage-intensive contracts.

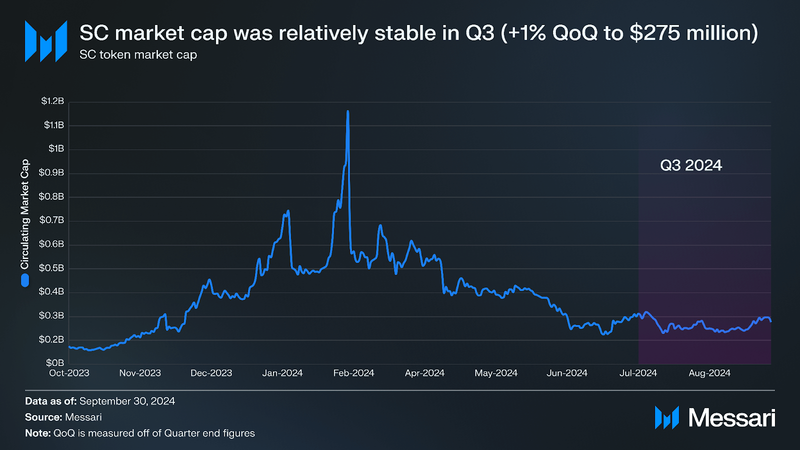

- Sia's market cap remained relatively stable in Q3’24, increasing by just 1% QoQ to $275 million despite broader market contractions.

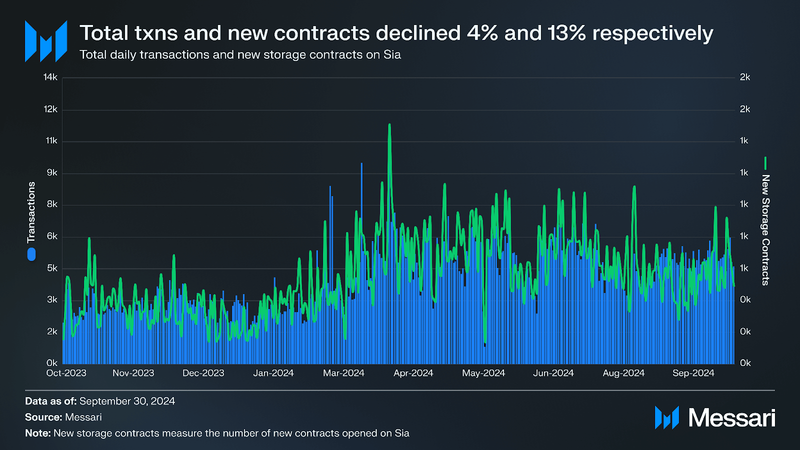

- New contract creations fell by 13% QoQ, leading to a minimal 4% QoQ decline in total transactions. The marginal decrease in total transactions suggests that network activity remained relatively stable and is mainly driven by ongoing activity from existing contracts and recurring payments.

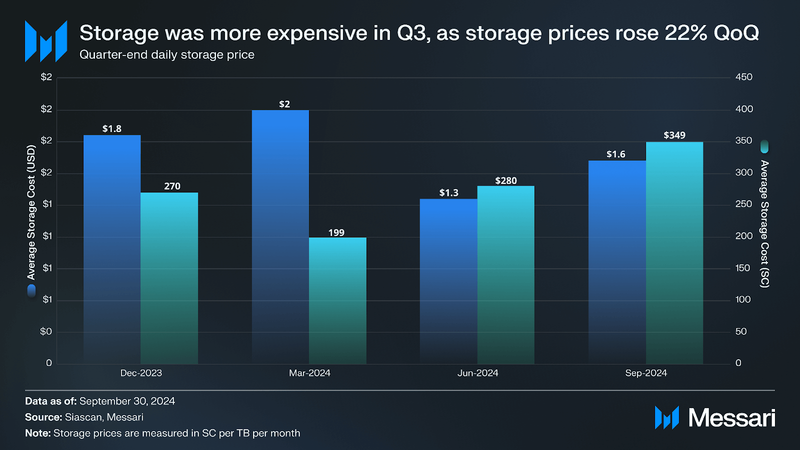

- Storage prices in USD rose 22% QoQ, reversing the downward trend from Q2’24. This rise in prices may have tempered demand for smaller storage contracts, contributing to the decline in total contracts and increase in higher-value storage deals with larger storage allocations.

- The Sia Ecosystem Grant Program saw notable progress in Q3’24, with grant recipients including DartSia, DeCast, Komodo, Lume Web, Sia NFS Gateway, and Fabstir achieving key development milestones.

Sia (SC) is a decentralized cloud storage network that combines a Proof-of-Work blockchain with a contract-based storage model. Storage contracts uphold storage agreements between hosts (storage providers) and renters(storage consumers). Renters define the amount of data to be stored, the timeframe for storage, and the price. As users and storage providers enter into storage contracts, they deposit the native asset — Siacoin (SC) — into an escrow account. Storage providers must cryptographically prove they are hosting the required data, and if they do not uphold the storage agreement, their collateral is slashed. At contract expiry, the storage provider receives most of the escrowed funds, with a small portion (3.9%) going to holders of Siafund (SF) tokens. Siafunds are security tokens that accrue SC to the SF holder from finished contracts on Sia.

Sia facilitates a global data storage marketplace by connecting storage providers with underutilized hard drive capacity to storage consumers. Siacoin can be used to pay for gas on the Sia blockchain and as the medium of exchange for the storage market. Renters pay a storage fee, upload/download bandwidth prices, and gas to create storage contracts. Files stored on the Sia network are encrypted via ChaCha20 and stored redundantly via Reed–Soloman Erasure Coding. Encryption ensures that uploaded files remain private, and redundancy ensures security by sharding files. Files uploaded to Sia are split into 30 or shards chunks and sent to various hosts. Only ten shards are required to rebuild the file, and their copies are re-duplicated to new hosts whenever one is offline. For a full primer on Sia, refer to our Initiation of Coverage report.

Website / X (Twitter) / Discord

Key Metrics Performance AnalysisTransactions and New Contracts

Performance AnalysisTransactions and New ContractsNew storage contracts are a measure of the origination of active storage contracts. New contracts require renters to allocate funds (called allowances) in advance. These allowances determine how much SC the renters are willing to pay for storage on Sia. The allowance is derived from an equation that multiplies the price in SC per TB stored by the expected number of TBs and by the expected number of months for storage. For example, if a user wanted to store 3 TB of data for three months at 500 SC per TB, their allowance would be 4,500 SC (500 SC x 3 TB x 3 months). Renters also pay contract formation and upload bandwidth fees when creating new contracts. Hosts must lock up collateral, which can be slashed if they don’t uphold the contract agreement.

Transactions on Sia account for all activity related to storage contracts, peer-to-peer transfers, and trades of the SC token. New contracts lead to various types of onchain transactions, such as contract initiation payments, bandwidth payments, and ongoing storage payments. For this reason, transaction count tends to be influenced by initiating new contracts. In Q3’24, new contract creations fell by 13% QoQ, leading to a minimal 4% QoQ decline in total transactions. This followed a strong Q2, where new contracts rose by 41% and transactions by 37%, suggesting Q3's slowdown was partly due to users concluding contracts initiated in previous quarters. Broader market contractions and an increase in storage cost (higher storage prices in USD terms) may have also reduced demand for storage, as fewer contracts were created in Q3. However, the 4% dip in total transactions suggests that network activity remained relatively stable and is mainly driven by ongoing activity from existing contracts and recurring payments.

Active ContractsWhen a contract is active, it automatically facilitates the exchange between escrowed SC and storage provided by hosts.

In Q3, active storage contracts declined by 5.4%, marking the first contraction in 2024. This drop may reflect the tapering effects of Q2’s growth, as fewer new contracts were initiated and older contracts expired. Additionally, the overall market contraction in Q3, despite improved user experience from incremental upgrades, may have dampened active contract growth.

Storage UtilizationWhile a storage network's capacity helps highlight its current scale, its utilization rate reveals the demand for the type of storage it optimizes for. Sia operates in the hot storage market, primarily targeting developers. It's favored by those searching for a decentralized storage system offering privacy and fast retrieval.

Storage demand on Sia flows through storage contracts, incentivized by its Stake-for-Access (SFA) token model. For this reason, storage demand is closely linked to active contracts. In Q3, storage usage rose 16.7% QoQ to 2,310 TB, reflecting a relative increase in the utilization rate. This suggests that the contracts initiated during the quarter involved larger storage allocations, likely reflecting a shift in user demand toward storage contracts requiring larger storage space.

Network RevenueSia produces revenue for multiple parties: hosts, miners, and Siafund (SF) holders. Its network revenue is the sum of payouts to hosts, Siafund fees, miner fees, and burned collateral. Burned collateral is included in revenue because burning SC makes it more scarce, accruing value to SC holders.

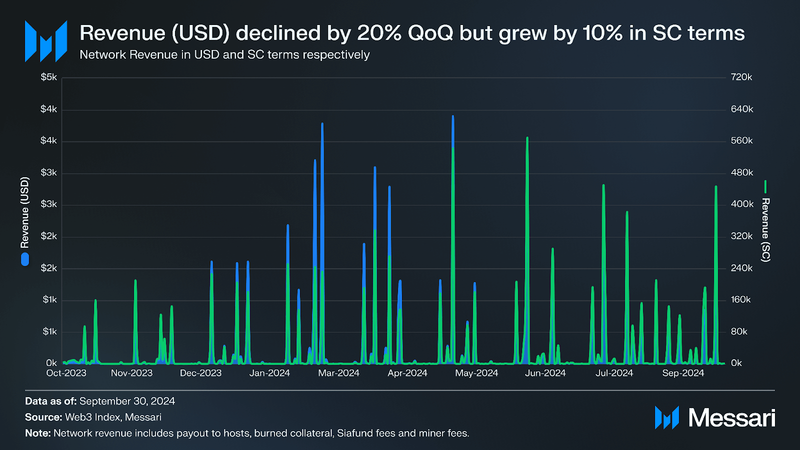

In Q3, Sia’s revenue decreased by 20% QoQ in USD terms but grew 10% in SC terms, reflecting the dual impact of market trends and network activity. The decline in USD revenue was likely driven by SC price volatility amid the broader crypto market weakness in Q3. However, the increase in SC-denominated revenue suggests that Q3 contracts were priced higher in value, likely attributed to larger storage allocations per contract. Regardless, Sia’s ongoing improvements to the network’s renting and hosting modules, with incremental upgrades throughout the quarter, helped maintain the network’s storage demand.

Storage PricesRenters entering a storage contract on Sia pay multiple fees to set up and maintain the contract. Storage fees are based on the amount of data uploaded, the length of the contract, and the price in SC per TB per month.

In Q3, storage prices in USD rose 22% QoQ, reversing the downward trend from Q2. This rise in prices may have tempered demand for smaller storage contracts, contributing to the decline in total contracts, while incentivizing higher-value storage deals with larger storage allocations. The increase likely reflects both stabilization in the SC market and sustained interest from users with larger storage needs.

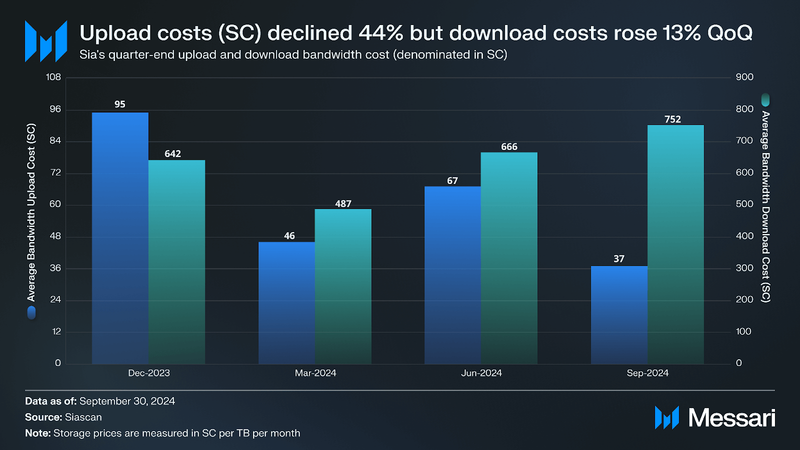

Bandwidth CostsStorage providers offload the costs of uploading and downloading the renter’s data to the individual renter. Users seeking to store data on Sia initially pay upload fees to hosts, and users seeking to retrieve uploaded data pay download fees to hosts. In both cases, bandwidth is priced per TB.

In Q3, upload costs in SC terms dropped 44% QoQ, while download costs rose 13% QoQ, reflecting shifting dynamics in storage provider pricing strategies. The decline in upload costs may indicate reduced demand for new data uploads, aligning with the decrease in new contract creations, while the rise in download costs suggests sustained or increased retrieval activity from existing users. These changes likely reflect storage providers balancing pricing to maintain competitiveness amid fewer new contracts while optimizing revenue from active renters requiring data access.

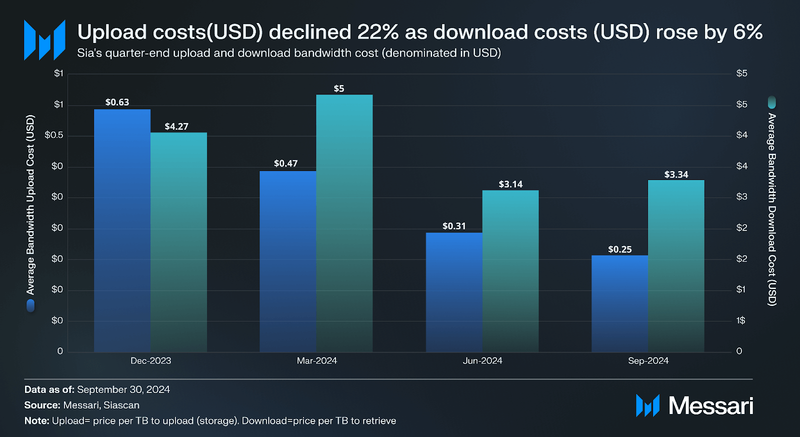

Similar to upload and download cost dynamics in SC terms, upload costs in USD terms declined by 22% QoQ, while download costs rose by 6%. The sharper decline in SC-denominated upload costs compared to USD terms in Q3 was likely due to SC's price volatility amid broader market contractions. As SC's value fell, users required significantly less SC to purchase the same storage and vice versa, amplifying the effect of cost reductions in SC terms. Conversely, the smaller changes in USD-denominated costs reflects stabilization efforts by providers to offset the volatility of SC's price and sustain revenue.

Market Cap

In Q3, Sia's market cap remained relatively stable, increasing by just 1% QoQ, despite broader market contractions. This stability contrasts with the sharp 53% drop in Q2, reflecting a possible recovery in market sentiment. The steadier market cap in Q3 may have contributed to less dramatic shifts in USD-denominated storage costs, as the SC price remained relatively consistent compared to the significant decline in Q2. However, SC-denominated costs for upload and download bandwidth still exhibited notable changes, with upload costs falling 44% QoQ and download costs rising 13% QoQ. This suggests that while token price stability reduced volatility in USD costs, the relationship between SC price, storage demand, and network dynamics continued to drive nuanced changes in pricing, with providers adjusting costs to align with user activity and maintain competitiveness.

Qualitative AnalysisSoftware UpdatesThroughout Q3’24, Sia modules renterd and hostd saw incremental upgrades that improved the network’s storage performance, usability, and reliability. These upgrades include the introduction of an account separation feature, webhooks for newly formed contracts, and enhanced account management. They also introduced UI modification features, including support for contract filtering and sorting and an improved configuration system.

Ultimately, Sia’s development focus remains the upcoming V2 hard fork (Utreexo), its first major upgrade since its mainnet launch in 2014. Among other proposed improvements to Sia, this upgrade will replace its traditional UTXO database with a cryptographic accumulator, reducing the initial sync time for nodes. This modification could scale Sia’s data storage and consensus code, enabling full nodes to run on smartphones, embedded devices, or even browsers.

Ecosystem Grant UpdateThe Sia Foundation continues to support ecosystem growth through its grant program. Since its inception, the grant program has approved a total of ~$1.6 million for projects spanning from development to research. The grants committee meets biweekly and consists of three Sia Foundation employees and three Sia community members. In Q3’24, the Foundation approved only $3,500 in small grant funding, marking its lowest funding quarter in 2024.

The approved grant was for Adrien Dalt to develop Darkola, an Orditb plugin that would integrate Sia’s decentralized storage capabilities into the popular OrbitDB system. This plugin enables decentralized applications to store and retrieve files using Sia’s network while maintaining the familiar interface of OrbitDB. As of Q3’24, the plugin package has been published on npm and has successfully passed functional tests.

Development Milestones

Throughout Q3’24, previously funded projects also achieved development milestones, some of which include:

- DartSia released login functionality, network overview, and host research features for its mobile application. These updates allowed users to access real-time network data, manage hosts, and perform basic file operations directly from the app.

- DeCast published its decentralized event management extension on Chrome and Firefox.

- Komodo Platform made progress in advancing the integration of Hash Time-Locked Contracts (HTLC) for atomic swaps to Sia with the testnet launch of Komodo’s AtomicDEX protocol. This release represents a key step forward in enhancing Sia's cross-chain transaction capabilities.

- Lume Web improved IPFS integration and billing management within its web app. While additional testing is planned, the team has laid the groundwork for enhanced UI and file management system updates. These steps bring the project closer to delivering a seamless decentralized web experience on Sia.

- Sia NFS Gateway released version 0.2.0, introducing the Cachalot content cache for chunking and deduplication. Version 0.3.0 followed, addressing compatibility issues on Windows and macOS, further improving accessibility and interaction with Sia-hosted files.

- Fabstir advanced its Web3 e-commerce platform with a permissioned/permissionless marketplace system that allows creators to set royalties and manage their assets. It also introduced a state machine system for NFT status tracking and blockchain events for marketplace transparency, boosting creator control.

Sia maintained steady performance in Q3’24, with a notable 16.7% QoQ increase in storage usage to 2,310 TB, driven by a shift toward contracts with larger storage allocations. Despite a slight 1% rise in market cap to $275 million, new contract creation declined by 13%, leading to a modest 4% decrease in total transactions. Revenue in SC terms grew by 10% QoQ, reflecting higher-value storage deals, though USD-denominated revenue fell 20%, impacted by broader crypto market conditions. Active contracts dropped by 5.4%, marking the first contraction of 2024, as fewer new contracts were initiated and older agreements expired.

Ultimately, Sia's development efforts remained strong, highlighted by the ecosystem’s progress through its grant program. Key projects included Fabstir’s advanced Web3 marketplace, DartSia’s mobile application updates, and Komodo’s cross-chain atomic swaps. Incremental updates to Sia’s renting and hosting modules improved network usability and performance, while preparations for the upcoming Utreexo hard fork signal a focus on Sia’s scalability and reliability.