and the distribution of digital products.

State of Bitcoin Q4 2024

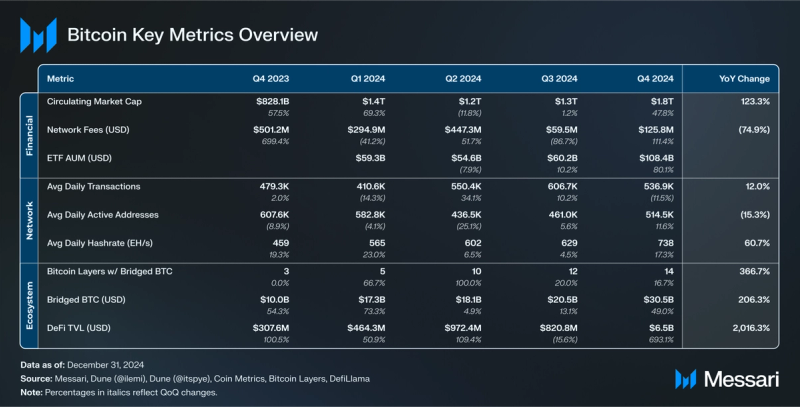

- BTC ended 2024 at $93,400, up 48% QoQ and 121% YoY. The rally was fueled by post-election market sentiment, increased institutional adoption, and aggressive BTC acquisitions by Strategy.

- Bitcoin ETFs also played a major role, with AUM surging 80% QoQ to $108.43 billion. BlackRock's IBIT became the most successful ETF launch in history, ending its first year with over $50 billion in AUM.

- Bitcoin’s mining industry thrived, with hashrate hitting a record 890 EH/s. Miner revenue surged 41% QoQ to $40.1 million, as BTC’s price growth offset the impact of halving. Mining difficulty increased by 15% QoQ, further reinforcing network security.

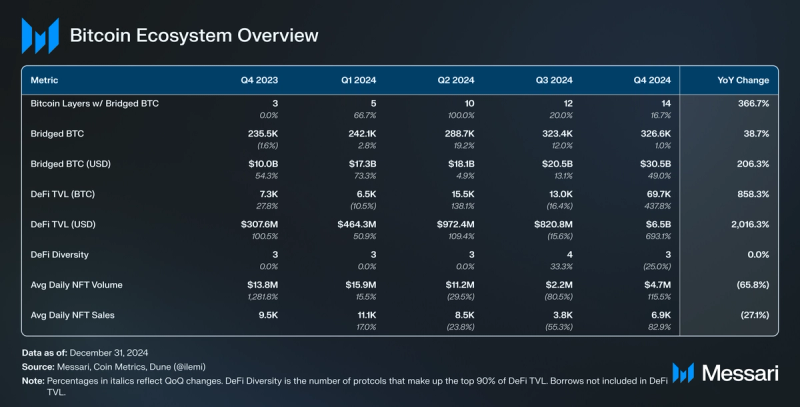

- Bitcoin layers and DeFi saw substantial growth. Bridged BTC rose 39% YoY to 326,600 BTC, while Bitcoin DeFi TVL increased 693% QoQ to $6.51 billion, ranking Bitcoin as the fourth-largest chain by TVL. Babylon led this expansion, capturing 82% of Bitcoin DeFi TVL.

- NFT activity rebounded, with trading volume up 116% QoQ to $4.7 million. Magic Eden maintained dominance, but OKX’s NFT marketplace rapidly gained market share, increasing volume by 281% QoQ.

Bitcoin (BTC) is the first distributed consensus-based, peer-to-peer payment settlement network. Bitcoin (BTC), the native asset of the Bitcoin blockchain, was the world's first digital currency without a central bank or administrator. Often referred to as digital gold, bitcoin has a predictable, stable monetary policy that operates autonomously, giving it the ideal store-of-value properties.

To secure its network, Bitcoin uses a Proof-of-Work (PoW) consensus mechanism to solve the “double-spend problem.” PoW requires participants (miners) to contribute computing power to solve arbitrary mathematical puzzles in order to add a new block to the blockchain. Bitcoin is awarded to the miner who solves the puzzle first, thus minting new bitcoins.

Bitcoin has historically been focused on enabling peer-to-peer payments and being a store of value, but not as much on DeFi, NFTs, and other narratives enabled by programmability (i.e., expressive smart contracts and arbitrary computation). Instead, those narratives were deferred to alternative networks. However, Bitcoin is now experiencing a renaissance of programmability, largely thanks to two recent innovations, Ordinal Theory and BitVM. Both innovations leverage offchain indexing or computation, and neither makes any changes to the core protocol. Ordinal Theory emphasized the demand for added functionality, and then BitVM made expressive and trust-minimized L2s seem possible. These innovations have sparked a frenzy of experimentation with onchain assets and modular layers.

Whitepaper / Reddit / GitHub

Key Metrics Financial Overview

Financial Overview Market Cap and ETFs

Market Cap and ETFs

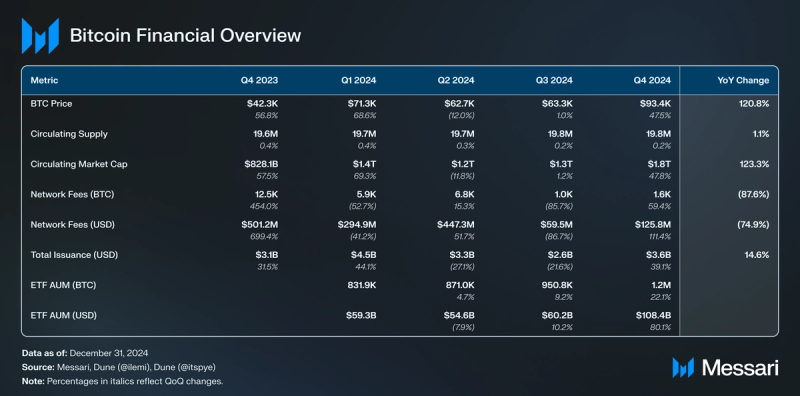

BTC capped off a bullish 2024 with an impressive Q4, ending the year at $93,400 (up 48% QoQ from $63,300 and up 121% YoY from 42,300). The US presidential election on November 5 kicked off a BTC rally that took it to multiple new all-time highs. A month later, on December 4, BTC hit $100K for the first time and eventually reached $108K before pulling back at the end of December. Strategy (formerly MicroStrategy) was one of the main drivers of this run-up, as they were aggressively acquiring BTC in Q4. On Oct. 30, announced its “21/21 Plan,” which aims to raise $42 billion in capital ($21 billion in equity and $21 billion in fixed income) over 3 years. After the election of Donald Trump, Strategy’s 21/21 Plan, alongside increased investor appetite, enabled it to almost double its BTC holdings from 252,220 in Q3 to 446,400 by the end of the year.

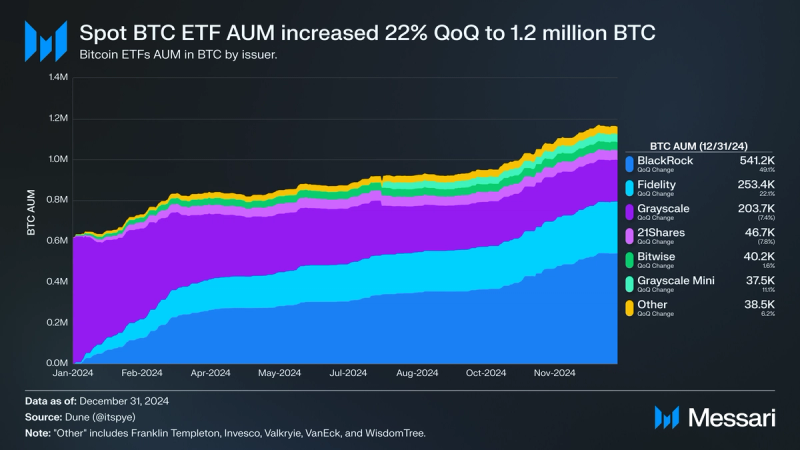

Alongside Strategy, the spot Bitcoin ETFs were another major driver of BTC price appreciation in Q4 and 2024. Spot Bitcoin ETF AUM in BTC increased 22% QoQ from 950,800 to 1.2 million BTC. The increase in USD was particularly even more impressive, as AUM increased 80% QoQ from $60.20 billion to $108.43 billion. Nearly half of all the AUM (47%) is held by Blackrock’s IBIT, which became the most successful ETF launch in history. IBIT’s BTC holdings increased 49% QoQ to 541,200. The second largest ETF, Fidelity’s FBTC, increased its BTC holdings by 22% QoQ to 253,400, representing 22% of all AUM. BTC in Grayscale’s GBTC decreased to 203,700, down 67% from 617,400 at launch. Furthermore, the outflows from GBTC decelerated in Q4 as its BTC holdings fell 7%, compared to -20% in Q3. Combined, IBIT, FBTC, and GBTC, hold 86% of all BTC in spot Bitcoin ETFs.

Supply Dynamics and Fees

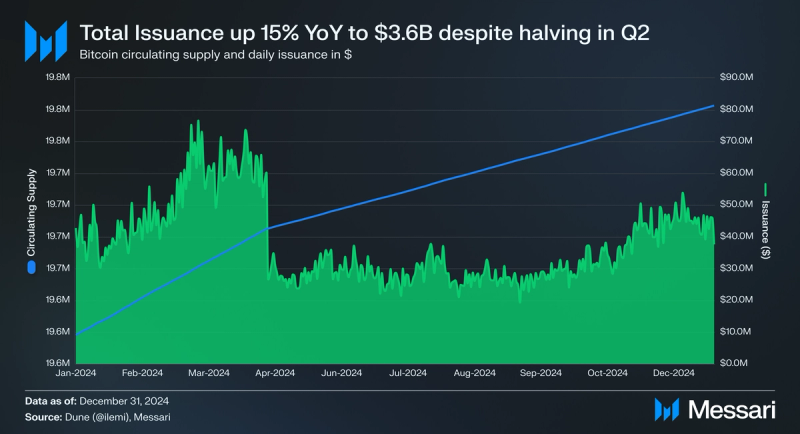

Bitcoin’s circulating supply increased by 0.2% QoQ to 19.8 million in Q4. For 2024, the circulating supply was up 1% YoY from 19.6 million. Until Bitcoin’s next halving in 2028, block rewards per mined block are 3.125 BTC. Total issuance in USD was up 39% QoQ from $2.56 billion to $3.56 billion, due to BTC’s price appreciation. However, total issuance was also up 15% YoY from $3.11 billion in Q4’23, despite BTC block rewards decreasing by half.

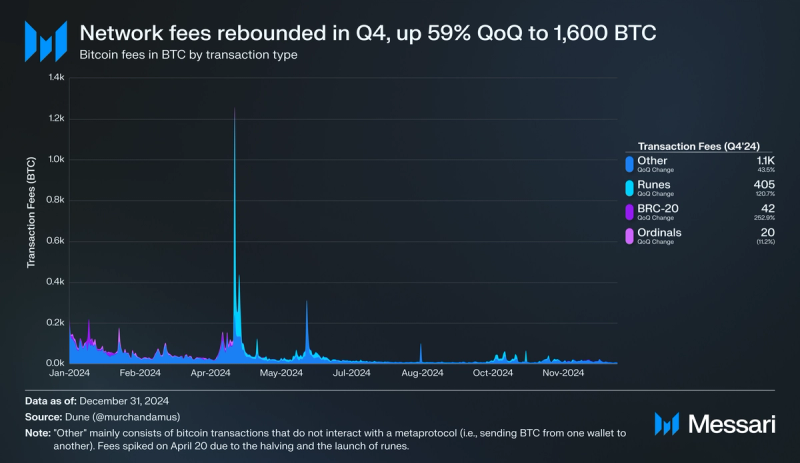

Network fees rebounded in Q4 after a slow Q3. Fees increased 59% QoQ from 1,000 to 1,600 BTC. In USD terms, the increase was even greater as it up 111% QoQ from $59.5 million to $125.8 million. Despite the growth in Q4, fees were down YoY in both BTC (-88%) and USD (-75%). However, Q4’23 was the height of inscription-related activity on Bitcoin, which resulted in elevated network fees. Compared to other L1s, only Ethereum ($550.0 million), Solana ($396.3 million), and TRON ($176.0 million) had more network fees in Q4.

Broken down by transaction type, the majority of network fees still come from “regular” transactions (i.e., sending BTC from one wallet to another). 70% of all transaction fees came from “regular” transactions, down 10% QoQ from 78% in Q3. Metaprotocols for fungible tokens, Runes and BRC-20, saw an increasing share of fees in Q4. Runes accounted for 405 BTC in fees (up 121% QoQ from 183 BTC), while BRC-20 accounted for 42 BTC in fees (up 253% QoQ from 12 BTC). Combined, runes and BRC-20 were 29% of network fees in Q4. Lastly, network fees from non-fungible ordinals fell 11% QoQ from 22 to 20 BTC.

Network Overview Onchain Activity

Onchain Activity

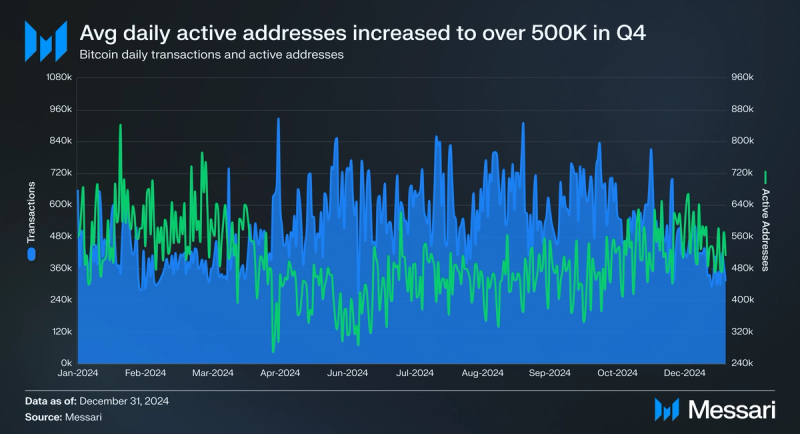

Onchain activity had mixed results on Bitcoin. Average daily transactions trended lower in Q4, down 12% QoQ from 606,700 to 536,900. Average daily active addresses, however, experienced an upward trend in Q4, increasing 12% QoQ from 461,000 to 514,500. Over the past year, average daily transactions (up 12% YoY from 479,300) and average daily active addresses (down 15% YoY from 607,600) trended in opposite directions.

Since the introduction of runes, Casey Rodarmor’s fungible Bitcoin token standard, their usage has largely displaced and surpassed that of the BRC-20 fungible token standard. Runes are often viewed as more economically viable considering BRC-20’s UTXO inefficiencies and have replaced them to become the most widely transacted Bitcoin alternative token standard. Despite these inefficiencies, BRC-20 transactions saw a resurgence in Q4, up 156% QoQ from 17,255 to 44,200. Popular BRC-20 tokens, such as ORDI and SATS, saw an increase in trading volumes in Q4, partially explaining the rise in BRC-20 transactions. Runes’ transactions trended in the opposite direction in Q4, falling 38% QoQ from 361,600 to 225,100. Because of this, “regular” transactions (up 20% QoQ to 263,200) surpassed runes as the main driver of transaction activity in Q4. Transactions that interacted with a metaprotocol (i.e., Ordinals, BRC-20, and Runes) were 47% of all transactions in Q4.

Bitcoin transaction fees are determined by the size of the transaction data (measured in bytes) and the number of transactions in the mempool. Daily average transaction fees in both BTC (up 79% QoQ to 0.00003 BTC) and USD (up 144% QoQ to $2.62) saw QoQ increases from Q3. Compared to Q4’24, transaction fees have come down significantly for both BTC (down 87% YoY) and USD (down 74% YoY), due to a decrease in ordinal-related transactions. Ordinal transactions typically consist of more transaction data than a normal Bitcoin transaction.

Mining

Hashrate represents the computational cost and resource demands faced by miners who secure the Bitcoin network. As hashrate increases, miner profitability decreases (assuming a constant BTC price and transaction activity). For Q4, the average daily hashrate increased 17% QoQ from 629 to 738 EH/s (exahashes per second). As for the entire year, the average daily hashrate is up 61% YoY from 459 EH/s. Furthermore, hashrate set new all-time highs in Q4, reaching 890 EH/s on November 19. For mining difficulty, it readjusts every 2,016 blocks (~2 weeks) based on the network’s hashrate. As such, the higher the hashrate, the higher the mining difficulty. Average daily mining difficulty increased 15% QoQ and 56% YoY to 100 T (trillion).

Miner revenue is the sum of all block rewards and network fees, denominated in USD. Since a miner’s costs are denominated in USD (electricity, equipment, land, etc.), miner revenue in USD must outpace mining costs for a miner to be profitable. Therefore, miner revenue increases with rising BTC prices and network fees. Additionally, each halving tends to have a negative impact on miner revenue as block rewards represent the majority of miner revenue. In Q4, average daily miner revenue increased by 41% QoQ from $28.5 million to $40.1 million. Block rewards represented 97% of miner revenue (down 1% QoQ), while network fees were 3% of miner revenue (up 50% QoQ). Lastly, average daily miner revenue was up 2% YoY from $39.2 million, signaling that BTC price has outpaced the negative effects of the halving in Q2.

Ecosystem Overview Layers

LayersOver the past year, Bitcoin has experienced a resurgence in demand and development activity for protocols scaling or adding increased functionality to Bitcoin. These protocols vary but are colloquially referred to as “Bitcoin layers.” According to Bitcoin Layers, an open-source platform that tracks the development and activity of these protocols, a Bitcoin layer is “a deliberately ambiguous term that encapsulates L2s, sidechains, state chains, and other networks 'aligned' with either bitcoin (the network) or BTC (the asset).“

For the purposes of this report, networks that support a bridged version of BTC have been split into three different categories:

- Alt L1s & More (i.e., Ethereum, Solana, Arbitrum, etc.) - Networks that support bridged version(s) of BTC, but the underlying network is sovereign from the Bitcoin network.

- Sidesystems (i.e., Stacks, Merlin, Core, etc.) - Networks that support bridged versions(s) of BTC and provide offchain execution for Bitcoin users.

- Bitcoin Native (i.e., Lightning Network) - Networks that support bridged version(s) of BTC and allow users to unilaterally exit the offchain system back to Bitcoin.

A more in-depth analysis of the difference between these categorizations can be found here. For the purposes of this report, Sidesystems and Bitcoin Native are both considered Bitcoin layers.

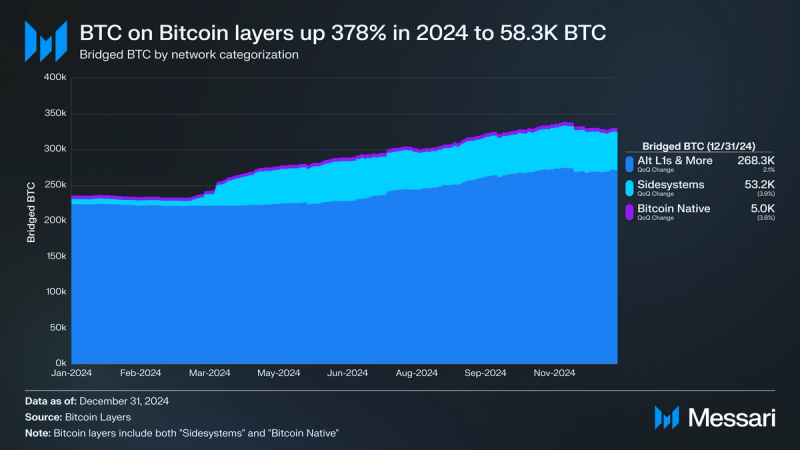

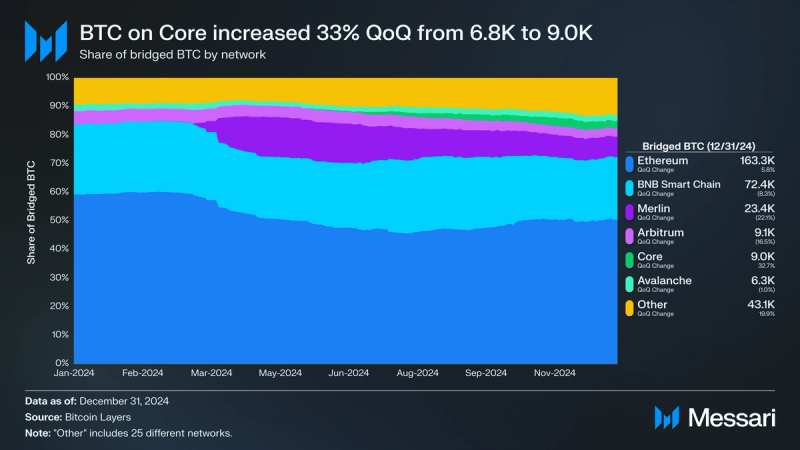

Bridged BTC across all networks increased by 1% QoQ from 323,400 to 326,600 in Q4. In USD terms, bridged BTC was up 49% QoQ from $20.47 billion to $30.50 billion. Broken down by category, Alt L1s & more was responsible for this growth as its bridged BTC increased 2% QoQ to 268,300. By the end of 2024, 82% of all bridged BTC was on alt L1s & more, 16% on sidesystems, and 2% on Bitcoin native networks. Zooming out for the entire year, there was considerable growth of bridged BTC on Bitcoin layers. Bridged BTC on Bitcoin layers was up 378% YoY from 12,200 to 58,300. For all networks, bridged BTC increased 39% YoY from 235,500.

By the end of 2024, there were 14 different Bitcoin layers with bridged BTC (up 2 from 13 in Q3):

- Merlin (Sidesystem) - Down 22% QoQ to 23,400 BTC

- Core (Sidesystem) - Up 33% QoQ to 9,000 BTC

- Bsquared Network (Sidesystem) - Up 59% QoQ to 5,500 BTC

- Lightning Network (Bitcoin Native) - Down 4% QoQ to 5,000 BTC

- Bitlayer (Sidesystem) - Down 29% QoQ to 4,000 BTC

- Liquid (Sidesystem) - Down 2% QoQ to 3,800 BTC

- Rootstock (Sideystem) - Up 3% QoQ to 3,100 BTC

- BOB (Sidesystem) - Up 126% QoQ to 2,800 BTC

- Stacks (Sidesystem) - Up 17% QoQ to 1,200 BTC

- Internet Computer (Sidesystem) - Down 30% QoQ to 200 BTC

- Rollux (Sidesystem - Q4 Launch) - 60 BTC

- Corn (Sidesystem - Q4 Launch) - 54 BTC

- BEVM (Sidesystem) - Down 23% QoQ to 22 BTC

- Libre (Sidesystem) - Down 41% QoQ to 2 BTC

Ethereum remained the network with the most bridged BTC, up 6% QoQ to 163,300 and 50% of all bridged BTC. Notably, other popular alt L1s and L2s lost market share, including BNB Smart Chain (-8% QoQ to 72,400 BTC & 22% of bridged BTC), Arbitrum (-17% QoQ to 9,100 BTC & 3% of bridged BTC), and Avalanche (-1% QoQ to 6,300 BTC & 2% of bridged BTC).

DeFi

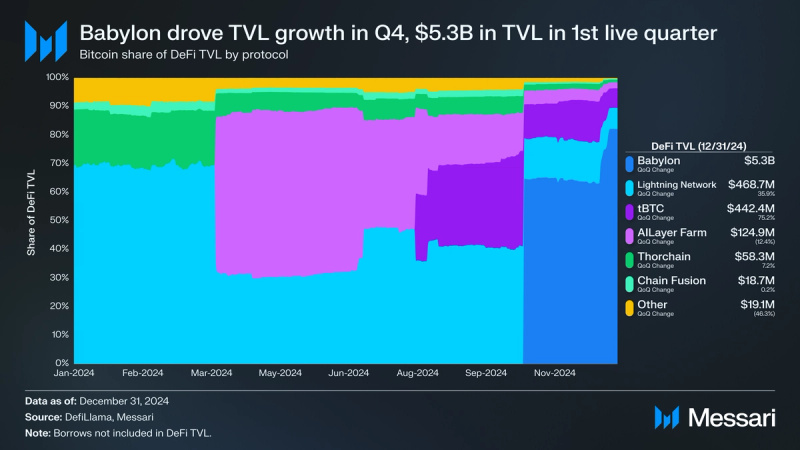

Bitcoin DeFi TVL denominated in USD, increased from $820.8 million in Q3 to $6.51 billion, a 693% QoQ increase. This ranked Bitcoin as the fourth-highest chain by TVL denominated in USD by the end of the quarter, rising 6 spots from 10 to 4. For 2024, TVL denominated in USD increased 2,016% YoY from $307.6 million. TVL denominated in BTC was also up in Q4, increasing 438% QoQ from 13,000 to 69,700 BTC. This dynamic indicates that the TVL increase in USD was driven by both capital inflows and the price appreciation of BTC.

In 2024, the Bitcoin DeFi ecosystem blossomed, with various new projects launching to expand DeFi and staking on Bitcoin. One protocol that has had an outsized influence on this growth is Babylon. Babylon is Bitcoin’s first staking protocol built directly on the Bitcoin network, offering a unique approach to leveraging Bitcoin's immense economic security. The protocol enables Bitcoin holders to stake their BTC, providing security for other networks in exchange for staking rewards. This system resembles Ethereum’s EigenLayer, with the caveat being that Babylon aims to harness Bitcoin’s $1.8 trillion market cap, making it an even more attractive asset for shared security. On Oct. 4, Babylon launched its points program for BTC staking, which helped it quickly capture TVL. By the end of the quarter, Babylon DeFi TVL stood at $5.29 billion (82% of DeFi TVL), making it the largest project on Bitcoin by TVL. Importantly, Babylon implements a phased approach to onboarding additional staked BTC. BTC was unable to be staked on Babylon after the end of Cap-3 in December.

Other protocols with notable TVL gains in Q4 was Lightning Network and tBTC. Lightning Network, an L2 payments channel built on top of Bitcoin, saw its TVL increase by 36% QoQ from $344.8 million to $468.7 million. Lightning Network’s share of TVL at quarter end was 7%, down 82% QoQ. tBTC is an ERC-20 token on Ethereum, backed 1:1 by BTC on Bitcoin, and is operated by Threshold. tBTC saw impressive growth in Q4, increasing 75% QoQ from $252.5 million to $442.4 million. Although, its share of TVL fell 77% QoQ to 7%.

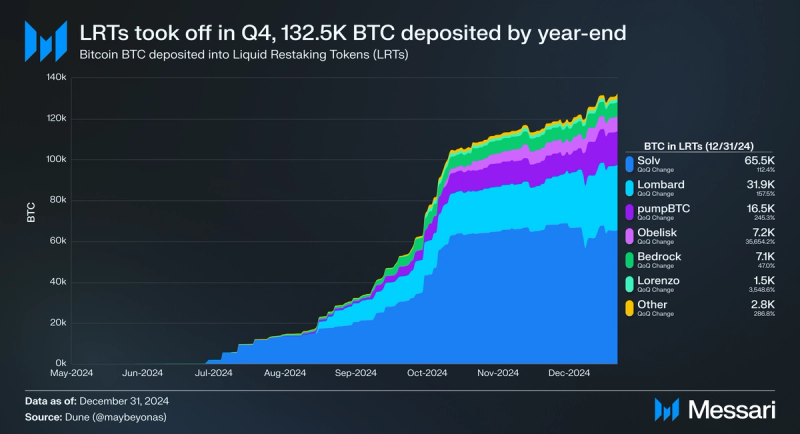

Liquid Restaking Tokens (LRTs) allow staked BTC to be restaked into Babylon and other restaking protocols, enabling native yield while maintaining liquidity and DeFi composability. Bitcoin’s restaking ecosystem has taken off alongside the rise of Babylon, with over 11 different live LRTs by year-end. BTC deposits in LRTs saw impressive growth in Q4, up 147% QoQ from 53,600 to 132,500 BTC. The most popular LRT by BTC deposited is Solv. BTC deposits in Solv grew 112% QoQ from 30,800 to 65,500. Furthermore, 49% of all BTC deposited in LRTs was in Solv. Solv benefited from its wide array of supported networks and DeFi integrations. After Solv, the next largest BTC LRT was Lombard. BTC deposits in Lombard increased 158% QoQ from 12,400 to 31,900. Lombard’s share of the BTC LRT market stood at 24% by quarter end. Similar to Solv, Lombard boasts a deep assortment of DeFi integrations. Rounding out the top 3 is pumpBTC, which saw its deposits increase 245% QoQ from 4,800 to 16,500. Combined, Solv, Lombard, and pumpBTC collectively held over 86% of the BTC deposited in LRTs.

NFTs

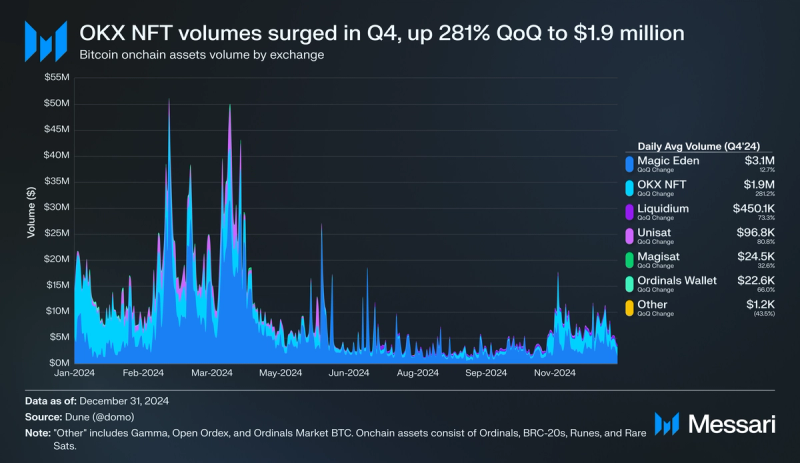

NFT activity rebounded back Q4 after a summer slump. As a result, the average daily NFT trading volume in Q4 increased 116% QoQ from $2.2 million to $4.7 million. Average daily sales also saw an increase, up 83% QoQ from 3,800 to 6,900. Compared to Q4’23, volume and sales were both down significantly, as the mania phase from inscriptions and ordinals has worn off. The popular NFT collection Quantum Cats (floor price up 47% QoQ to 0.37 BTC) was the best performer amongst the large-cap Bitcoin NFT collections in Q4.

Broken down by exchanges, Magic Eden once again accounted for the majority of onchain asset volume. Its daily average volume increased 13% QoQ from $2.7 million to $3.1 million. Notably, its share of onchain asset volume fell 28% QoQ to 55%, primarily due to OKX’s NFT Marketplace. Its daily average volume increased 281% QoQ from $506,600 to $1.9 million, representing 35% of onchain asset volume in Q4 (up 143% QoQ). The only other exchange that averaged over $100K in daily average volume was Liquidium. Liquidium is a lending platform that allows users to borrow BTC against onchain assets such as ordinals, BRC-20s, and runes. Daily average volume on Liquidium increased 73% QoQ from $259,700 to $450,100. Combined, Magic Eden, OKX’s NFT Marketplace, and Liquium accounted for 97% of onchain asset volume in Q4 (flat QoQ). The top five exchanges by daily average onchain asset volume are as follows:

1. Magic Eden - $3.1 million (up 13% QoQ)

2. OKX’s NFT Marketplace - $1.9 million (up 281% QoQ)

3. Liquidium - $450,100 (up 73% QoQ)

4. UniSat - $96,800 (up 81% QoQ)

5. Magisat - $24,500 (33% QoQ)

Closing SummaryBitcoin concluded one of its most impactful years to date with substantial growth across many key metrics in Q4. BTC’s price surged 121% YoY to $93,400, driven by institutional adoption, ETF inflows, and strategic acquisitions. Spot Bitcoin ETFs saw massive adoption, with AUM reaching $108.43 billion, while Strategy significantly expanded its BTC holdings. Network activity presented a mixed picture, as daily transactions declined but active addresses increased, alongside a resurgence in BRC-20 and Runes transactions. Meanwhile, rising fees and record-breaking mining hashrate underscored the network’s economic security.

Bitcoin’s DeFi and scaling ecosystem experienced significant expansion, with DeFi TVL soaring 693% QoQ to $6.51 billion, fueled by protocols like Babylon. NFT trading volumes recovered, led by Magic Eden and a growing presence from OKX’s NFT marketplace. With surging institutional adoption, evolving network functionality, and expanding Bitcoin-native financial applications, Bitcoin is positioned for continued growth and innovation in 2025.